Fintech | Robo-advisors | Bitcoin | Blockchain | Insurance

I look at the current state of play, the rise of the robo-advisor as well as disruption in payments, AI and insurance.

Subscribe to my newsletter to see content first:

This week is all about fintech thanks to a request from Jo (HT!). I look at the current state of play, the rise of the robo-advisor as well as disruption in payments, AI and insurance. Read on dear audience.

Is fintech running for the hills?

Fintech is clearly important to the UK. London is seen as a global financial centre and a place for innovation so naturally it should aim to lead here. The government clearly agreed and commissioned EY all the way back in 2014 to look at the opportunity.

A lot has changed since then though. After three years, we have seen the start of brexit and a large number of finance jobs shift to Europe.

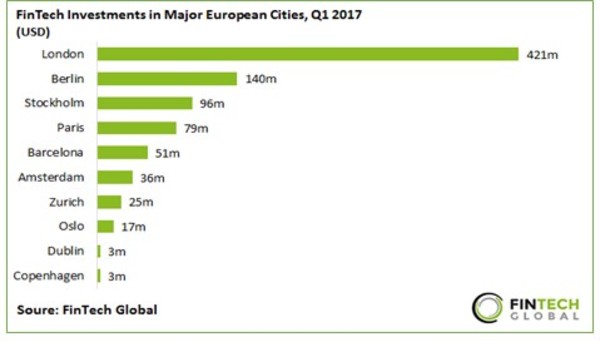

Things are not looking bad for fintech though. Research from Fintech Global suggests London was still leading the way in Europe in terms of overall investment.

There is a view that brexit does not hurt fintech outside of issues that are hitting startups across the board (investment and hiring for the most part). Certainly the fintech companies themselves are reporting stellar growth with many suggesting revenues will double over the next 12 months.

The Financial Conduct Authority (FCA) is really the key driver behind the success of fintech in the UK. Its focus on innovation and openness, illustrated by the focus on increasing global integration especially with China, South Korea and India suggest that fintech should still thrive in London.

Work the FCA has done with Lithuania to fast track approvals has been taken advantage of by London-based Revolut, one of the most hyped business banks allowing low cost multicurrency banking.

New faces

For years most of the innovation has been on the consumer payments and peer to peer lending. The biggest fintech companies are in this space but increasingly these companies and new entrants are looking to service businesses as well. Transferwise recently announced its borderless account aimed at businesses and aiming directly at new entrant Revolut.

Newer fintech entrants have seen their focus shift elsewhere. Alongside business banking, there has also been a rise in consumer bank accounts, wealth management platforms and insurance.

Perhaps the area that has grabbed worldwide attention the most though is bitcoin and its underlying technology blockchain (which you can think of as a public ledger of all transactions).

Last week, the value of a bitcoin powered through the $5000 mark, its highest ever and up 350% since the beginning of the year coming through some significant hurdles thanks to a civil war between the groups managing the digital currency. I discussed this in more detail here.

Since that peak, the price has fallen 20% going below $4000 in a week. This seems to be due to the Chinese government suggesting it is going to close down the exchanges in China, a huge market for bitcoin trading.

Separate to this China has also banned Initial Coin Offerings (ICOs). These are the latest vehicle for companies to raise money and they have been unregulated. You can read my previous commentary here as well as an excellent look by venture capitalist, Fred Wilson on the differing approaches of US and China and what it means.

Robo fintech

It should not be a surprise to see artificial intelligence make an appearance inside fintech. With so much data available from which to make decisions about things like spending habits and investment, the challenge has been working with the right data and in a timely fashion.

The largest players here are the investment companies (Nutmeg, Scalable Capital etc.) who have now grown large enough to be invested in by some of their larger and more traditional incumbents.

When it comes to your own everyday finances, Plum and Squirrelwere good mobile versions of traditional savings approaches, whilst Moneybox was a more innovative way of making you save without realising by rounding up the cost of items and squirreling away the difference. Nothing very intelligent though.

Last week, US based Pefin announced it is using artificial intelligence to help people make better financial decisions when it launches later in the year. The challenge is it needs three months worth of spending data to get started though we are not far away from EU regulations forcing the banks to open up access to this data (the UK is also going to adopt these regardless of Brexit).

Insurance with a conscience

One of the most profitable and complex industries is insurance but there is plenty of innovation happening. The most well known of these is Lemonade, which is focusing on reducing premiums, donating to charity and increasing transparency. Oh and it also uses artificial intelligence.

It makes money by keeping 20% of all premiums and sets aside 40% for insuring itself against major claims with the remaining 40% covering claims.

Unlike traditional insurance companies, any money not used for claims then goes to a charity of a customer’s choice. It has captured the imagination of consumers though still small and only available in a few states in the USA. After the first year though, it delivered $53,174 or 10.2 percent of first year revenues.

Where does it use AI? In chatbots, using them to automate customer interactions, though not many actually complete without human intervention. It is a mobile first company so its primary interface is through its mobile app though it does have a website.

If it succeeds in getting the chatbots to take over a large percentage of customer interaction, the company would be attractive to existing insurance companies regardless of the success of its business model. Of course, the insurance companies may want to try and buy the company and shut it down if it becomes too successful and undermines their very profitable current model.

The model is inspiring other insurance startups to adopt a similar approach. A new yet to launch pet insurance company in the UK is looking to follow a similar model and I would be very surprised if there weren’t others.

About Riaz

I've spent over 20 years building and scaling B2B products, services and marketing technology - from early-stage startups through to exits, and now as CEO of Radiate B2B - the B2B ad platform.

Along the way I've led teams, launched products, built and sold companies, and spoken around the world about data, AI and the future of marketing and work.

Today I split my time between working directly with companies as a consultant and fractional operator, mentoring founders and leaders, and speaking to audiences who need someone to translate what's happening in technology into decisions they can act on.

Read the full storyRecommended posts

The future of innovation, startups and the world. That's all.

I'll reflect on both in the next week or so I suspect but this week's newsletter looks at innovation, the business of looking into the future, how.

Read moreStrawberry picking robots, winning users and societal challenges.

This week returns to strawberry picking robots, overcoming inertia to win users and the challenges of user generated content for children and wider.

Read moreTech, politics and privacy. Where next?'

This week looks at the big technology firms, privacy and politics; Are we doomed to end up in nineteen eighty four.

Read more